Life insurance has long been viewed as a cornerstone of financial planning, yet for many individuals and families, it remains out of reach—either due to cost, complexity, or lack of awareness. Making life insurance affordable and accessible is not just a matter of pricing; it’s about reshaping how the industry engages with consumers, designs products, and delivers value. In a world where financial security is increasingly fragile, ensuring that more people can protect their loved ones through life insurance is both a social imperative and a business opportunity.

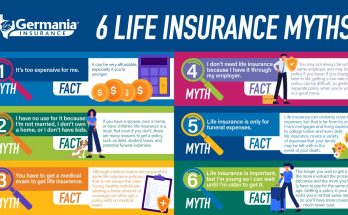

Affordability begins with understanding. Many people assume life insurance is expensive, often overestimating the cost by a wide margin. This misconception can deter individuals from even exploring their options. In reality, term life insurance—one of the most straightforward and cost-effective forms of coverage—can be surprisingly affordable, especially for younger applicants in good health. For example, a healthy 30-year-old might secure a substantial policy for less than the cost of a weekly coffee habit. But without clear, accessible information, these facts remain buried beneath layers of industry jargon and outdated assumptions.

Accessibility, meanwhile, hinges on simplicity and transparency. Traditional life insurance applications can be lengthy and invasive, requiring medical exams, detailed questionnaires, and weeks of underwriting. For many, this process feels daunting and unnecessary, especially in an age where digital services are expected to be fast and frictionless. Insurers that streamline the application process—using data analytics, simplified underwriting, and online platforms—are making it easier for people to get covered without sacrificing quality or reliability. When someone can apply for life insurance from their phone in under 15 minutes, the barrier to entry drops dramatically.

Technology is playing a transformative role in both affordability and accessibility. Digital platforms allow insurers to reach underserved populations, offer personalized quotes, and educate consumers in real time. Algorithms can assess risk more efficiently, reducing administrative costs and enabling more competitive pricing. Mobile apps and chat-based interfaces make it easier for users to understand their coverage, update beneficiaries, and manage policies without needing to navigate complex paperwork or wait on hold. These innovations are not just conveniences—they’re catalysts for inclusion, bringing life insurance into the hands of people who might otherwise be left out.

Education is another critical piece of the puzzle. Many people don’t buy life insurance simply because they don’t understand it. They may not know the difference between term and whole life, or they may be unsure how much coverage they need. Financial literacy campaigns, employer-sponsored workshops, and community outreach programs can help demystify life insurance and show how it fits into broader financial goals. When people see life insurance not as a luxury but as a practical tool for protecting their families, they’re more likely to engage with it proactively.

Affordability also depends on flexibility. Life insurance products that allow for customization—adjustable coverage amounts, optional riders, and scalable premiums—can meet a wider range of needs and budgets. For instance, a young parent might start with a modest term policy and later add coverage as their income grows or their family expands. Offering modular products that evolve with life stages makes insurance more relevant and sustainable. It also encourages long-term relationships between insurers and policyholders, fostering trust and loyalty.

Inclusivity is equally important. Historically, certain groups—such as low-income families, gig workers, and individuals with pre-existing conditions—have faced barriers to obtaining life insurance. Addressing these disparities requires thoughtful underwriting, community engagement, and a willingness to challenge outdated norms. Some insurers are now exploring alternative data sources, such as pharmacy records or wearable device metrics, to assess risk more fairly and expand access. Others are partnering with employers, unions, and nonprofit organizations to offer group coverage or subsidized plans. These efforts reflect a broader shift toward equity and social responsibility within the industry.

Regulatory support can also help make life insurance more accessible. Governments and oversight bodies play a role in ensuring that products are fair, transparent, and available to those who need them most. Incentives for insurers to serve underserved markets, guidelines for clear disclosures, and protections against discriminatory practices all contribute to a healthier, more inclusive insurance landscape. Collaboration between public and private sectors can amplify impact, especially when it comes to reaching rural communities or populations with limited digital access.

Ultimately, making life insurance affordable and accessible is about meeting people where they are—financially, emotionally, and technologically. It’s about recognizing that behind every policy is a story, a family, and a future worth protecting. When insurers prioritize empathy, innovation, and education, they don’t just sell products—they build relationships and deliver peace of mind. In doing so, they help ensure that life insurance fulfills its true purpose: providing security, dignity, and continuity in the face of life’s uncertainties. As the industry continues to evolve, the challenge is not just to expand coverage, but to do so in a way that is meaningful, inclusive, and enduring.